Le Crunch

A credit crunch is upon us.

2023 is fast becoming the year in which the stark realities of the end of the easy money era are becoming visible. There was already evidence that lending was being curtailed but the recent banking wobbles have exacerbated the process.

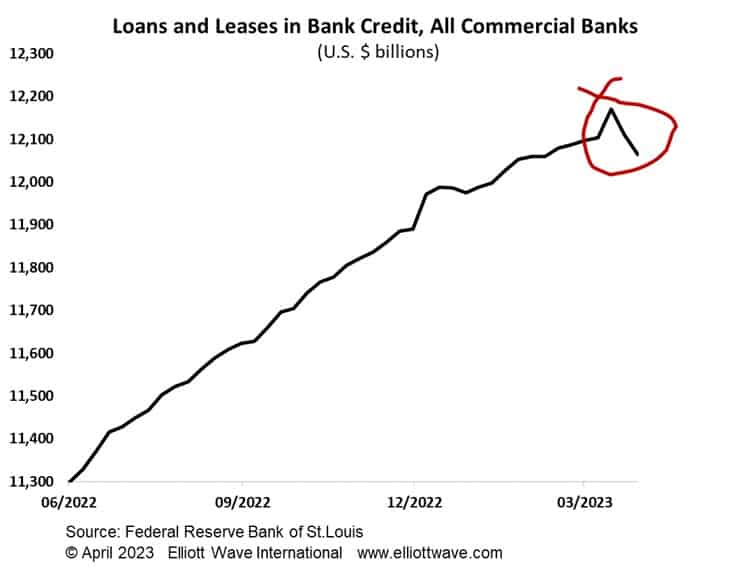

The chart below shows the amount of loans and leases in bank credit from U.S. commercial banks. The series has just witnessed the biggest two-week drop in the history of the series going back to 1973. The contraction in credit was across all sectors, from real estate to commercial and industrial loans.

In Europe, the last bank lending survey from the European Central Bank showed that banks tightened lending standards by the most since 2011. That was in the last quarter of 2022 and it’s very probable that the lending has been even more curtailed in the first few months of this year.

In the U.K., meanwhile, 56,000 2-year fixed rate residential mortgages are due to expire this summer leaving borrowers with much higher rates when they re-set. Expect to see consumer demand dampened as a result.

The shock of tighter money is really only just beginning.