Gold, Inflation & Deflation

Consumer price inflation is up but Gold is down. That’s not unusual.

Gold, they say, is the ultimate consumer price inflation hedge. The famous story goes that a Roman strutting his stuff down Via Sacra back in Emperor Nero’s day nearly two thousand years ago would have paid an ounce of gold for his top-of-the-market toga, sandals and belt. In 2021, with the euro price of Gold hovering just above €1,500, a chic Roman posing down Via del Corso would have paid that for his Salvatore Ferragamo designer suit, his Gucci shoes and accoutrements.

Gold bugs point to this as evidence that Gold is the ultimate currency because it has held its store of value for millennia. Whilst that may be true, shorter time frames reveal a rather messy picture.

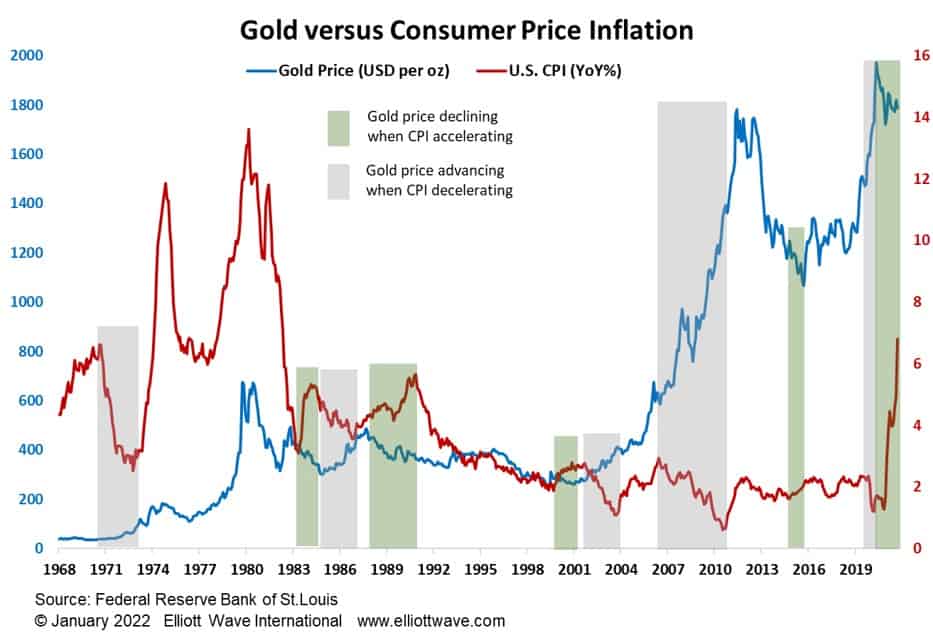

The chart below shows the U.S. dollar price of Gold versus the annualized rate-of-change in the U.S. Consumer Price Index (CPI). If you believe in Gold as a consumer price inflation hedge then, as the CPI is accelerating, the Gold price should be advancing. The green shaded areas show that there have been five occasions since 1980 when the opposite was true, the last year being a good example. On the other side, the Gold-Inflation myth would allude to the price of Gold declining as CPI was decelerating. The grey shaded areas show five occasions since 1970 when this was not the case, 2007 to 2010 being a prime example.

In fact, the correlation coefficient between the two series turns out to be MINUS 0.43, meaning that not only does no relationship appear to exist, if any does, it’s a negative one. I can hear my old econometric lecturer asking if we’re comparing apples and apples. Well, I suppose we could look at the correlation between the annualized rate-of-change between both series. That turns out to be 0.41. Positive, at least, but still no evidence of a relationship. Even being generous and comparing the Consumer Price Index itself (which, of course, has risen inexorably) with the price of Gold gives a correlation coefficient of 0.83. Much better but more akin to the Roman story than anything else. The evidence suggests that, whilst Gold might go up over the long-term as the CPI chronically advances, shorter time frames, which can last years, suggest no relationship at all.

“Poppycock!” the gold bugs say, “Gold goes up whether we have inflation or deflation.” It’s true, consumer price deflation during an economic collapse such as in the 1930s may well see the free-market price of Gold advance as people seek it as a survival hedge. During the Great Depression, the fixed price went up from $20.67 to $35 per ounce. But this was a blatant devaluation of the U.S. dollar by the government, not because people were buying Gold; they weren’t allowed to, and, anyway, FDR had stolen their holdings.

In conclusion, therefore, the recent relationship between Gold and the CPI has not been unusual in an historic context. What happens next? Thankfully, Gold is a free market these days, so the Elliott waves should guide us. Stay tuned.